Beginner-Friendly Intro to Algorithmic Trading

You’ve probably seen the ads.

“Turn $100 into $10,000 with this algorithmic trading strategy.”

“Quit your job and trade full-time.”

“My bot makes $500 a day on autopilot.”

That is not how algorithmic trading actually works.

Algorithmic trading is not a shortcut to wealth. It is a structured, rules-based approach to trading that relies on testing, discipline, and realistic expectations. When done properly, it replaces impulsive decision-making with repeatable processes.

In this guide, we’ll cover what algorithmic trading really is, how it works in practice, what beginners actually need to get started, and what outcomes are realistic over time.

What algorithmic trading really means

Algorithmic trading (also called algo trading or systematic trading) means using a predefined set of rules to make trading decisions instead of relying on intuition, opinions, or emotions.

Instead of thinking:

“This stock looks cheap.”

“I feel the market will go up today.”

“Someone recommended this trade.”

You define explicit rules such as:

Buy when RSI is below 30 and price closes above the previous day’s high.

Sell when profit reaches 10 percent, loss reaches 5 percent, or after a fixed number of days.

The key distinction is that the rules are written down, testable, and repeatable.

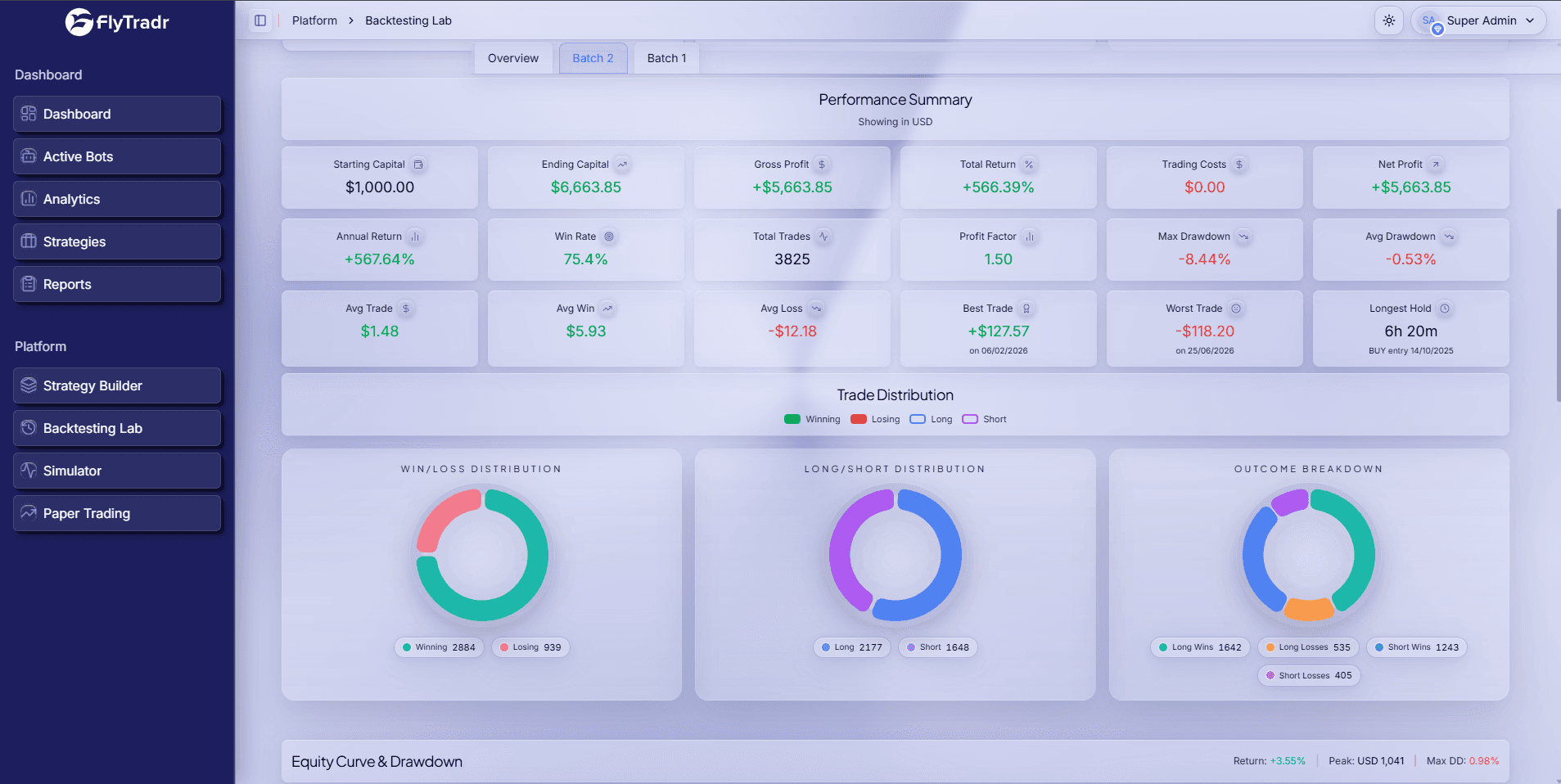

Because of this, you can test strategies on historical data, measure performance objectively using metrics like drawdown, win rate, and Sharpe ratio, and execute trades consistently without emotional interference.

What algorithmic trading is not

It is not a money-printing machine.

Most viable strategies operate within realistic statistical limits. Many strategies that survive real-world conditions produce Sharpe ratios roughly between 0.5 and 2.0. In practical terms, this often translates to moderate annual returns accompanied by regular drawdowns and losing periods. Losses are not a sign of failure; they are part of the distribution.

It is not “set and forget.”

Strategies require ongoing oversight. Markets evolve, liquidity conditions change, and assumptions can break. Responsible traders review performance periodically, revalidate assumptions, and adjust risk controls when necessary. A strategy that worked years ago may degrade or stop working entirely.

It is not limited to quants or PhDs.

You do not need an advanced math degree, deep programming expertise, or large amounts of capital to begin. What you do need is a willingness to learn, the discipline to follow predefined rules, and patience to let results play out over time.

How algorithmic trading works in practice

The process generally follows a sequence.

First, you define a strategy.

You start with a hypothesis, such as the idea that prices often revert after sharp declines. That hypothesis is converted into precise entry, exit, and risk rules. Nothing is left open to interpretation.

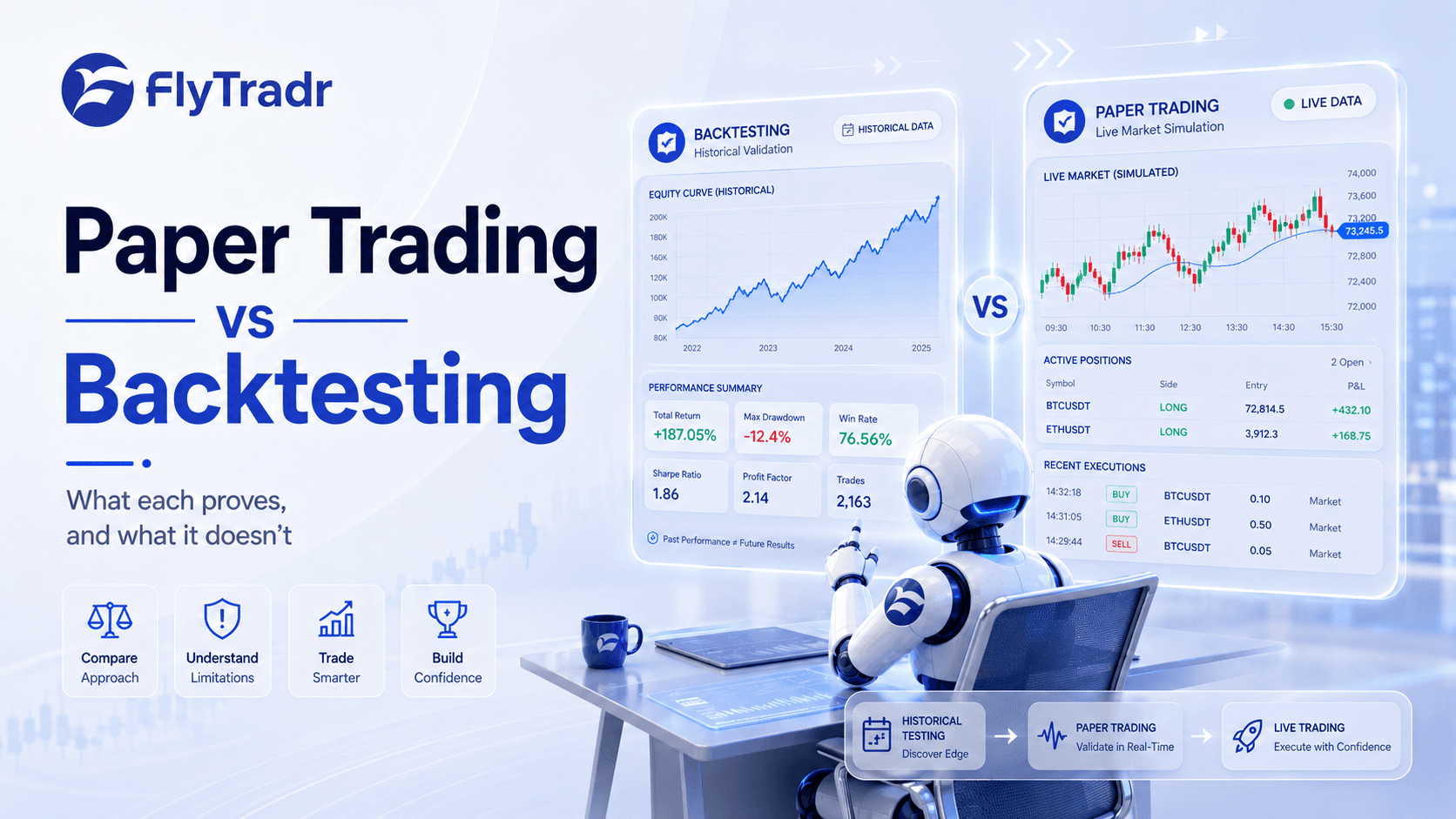

Second, you backtest the strategy.

Backtesting involves applying the rules to historical data to evaluate how the strategy would have behaved. You analyze returns, drawdowns, trade frequency, and consistency. Backtesting does not prove future performance, but it helps eliminate weak ideas early.

Third, you validate using walk-forward testing.

Instead of optimizing rules on all historical data at once, you test them in rolling periods. This reduces the risk of overfitting, where a strategy performs well only because it was tuned too precisely to past data.

Fourth, you test in a simulator.

A simulator replays historical data as if it were happening live. This allows you to observe trade sequencing, execution behavior, and psychological reactions without financial risk.

Fifth, you paper trade.

Paper trading runs the strategy on live market data using simulated capital. This step helps confirm that execution logic, data feeds, and broker behavior align with expectations.

Finally, you go live cautiously.

When real capital is involved, position sizes are kept small initially. Real-world trading introduces emotional pressure that cannot be fully simulated. Scaling happens gradually and only if results align with expectations.

Common types of algorithmic strategies

Trend-following strategies aim to capture sustained price movements. They tend to have lower win rates but larger individual winners. Sideways markets can be challenging for them.

Mean reversion strategies assume prices revert toward an average after extreme moves. They often have higher win rates but require strict risk control to prevent large losses during strong trends.

Breakout strategies attempt to capture momentum when prices move beyond established ranges. They can generate strong returns during volatile periods but also suffer from false signals.

Each category has trade-offs. None are universally superior.

What beginners realistically need

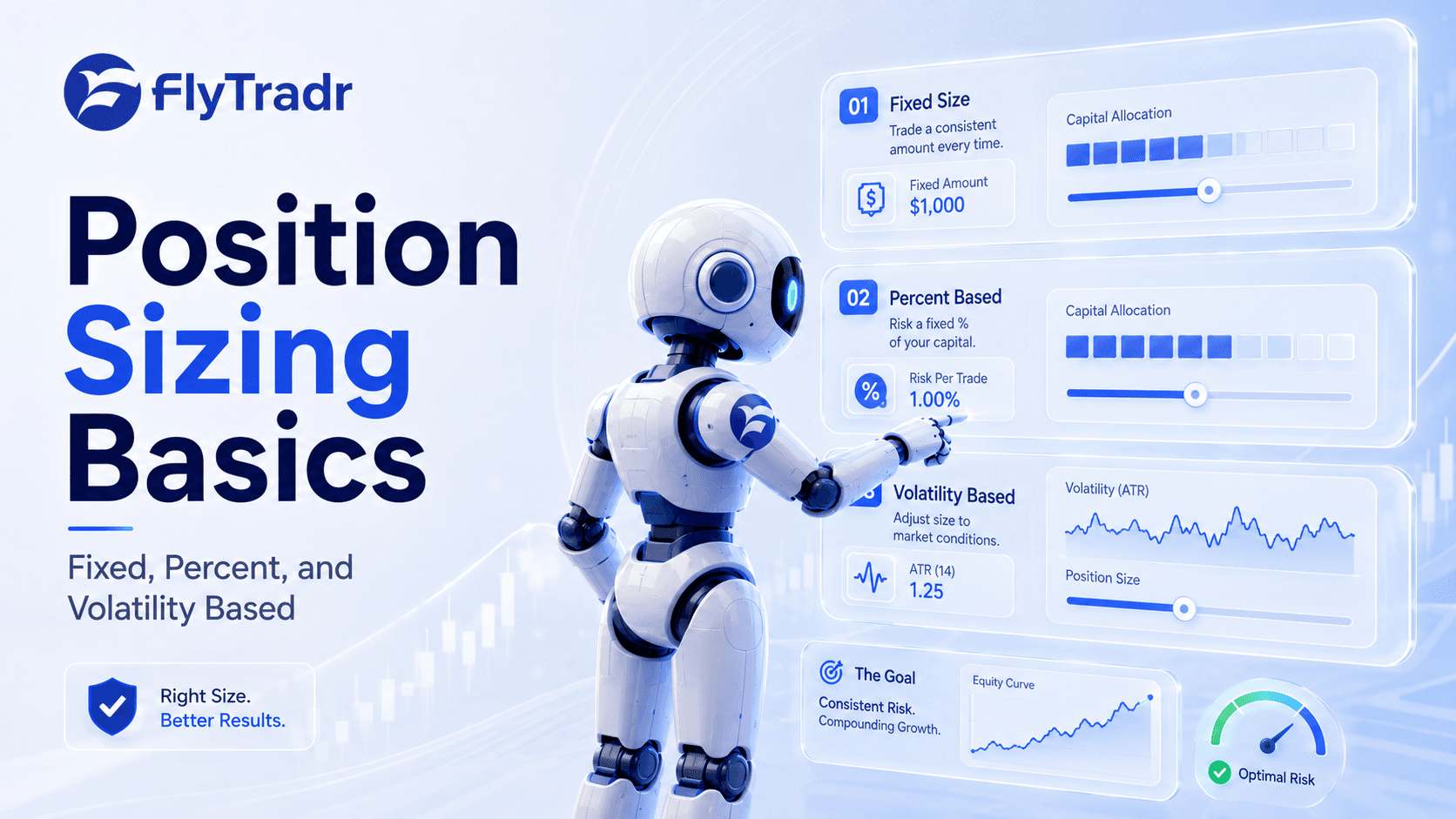

Capital requirements depend on market, timeframe, and costs. Smaller accounts can work but often require longer timeframes and conservative sizing to avoid being overwhelmed by commissions and slippage.

Tools are essential. At a minimum, traders need reliable historical data, backtesting capability, and a broker for execution. Coding is optional; no-code platforms can handle many use cases.

Time commitment matters. Algorithmic trading is not passive income. Even systematic strategies require regular monitoring, review, and maintenance.

Temperament is critical. Discipline, patience, and emotional control often matter more than strategy selection. Many failures occur not because the strategy was flawed, but because the trader abandoned it during normal drawdowns.

Realistic expectations over time

The first year is typically focused on learning. Many beginners break even or achieve modest gains while building foundational skills.

The second year is about refinement. Traders narrow their focus to fewer strategies, improve execution, and manage risk more deliberately.

Long-term success looks like steady, compounded growth with controlled drawdowns. It is rarely spectacular, but it is sustainable when done correctly.

Common beginner mistakes

Over-optimizing parameters to past data creates fragile strategies that fail in live markets.

Ignoring transaction costs leads to inflated backtest results.

Abandoning strategies after short-term losses prevents meaningful evaluation.

Deploying too many strategies at once dilutes focus and accountability.

A practical learning roadmap

Learning algorithmic trading works best when approached incrementally. Start with simple strategies, test them thoroughly, observe behavior in simulation, and only then move toward live deployment. Progression matters more than speed.

The bottom line

Algorithmic trading is a disciplined, test-driven approach to markets. It replaces emotional decisions with process. It is not passive income, guaranteed profit, or a shortcut to wealth.

What it offers is structure, repeatability, and the ability to learn systematically from both success and failure.

There is no secret strategy. There is only a repeatable cycle: define rules, test them, validate assumptions, deploy cautiously, monitor results, and adjust when necessary.

That process is learnable. It is not glamorous. But over time, it is how durable trading systems are built.

Comments

Ask a question or leave feedback. Guests can post too.

Max 2000 characters.

No comments yet.

Quick answers

What is this article about?

Algorithmic trading isn't a get-rich-quick scheme.

Who should read this article on A Beginner-Friendly Intro to Algorithmic Trading (Without Hype)?

This article is for retail traders who want a practical understanding of a beginner-friendly intro to algorithmic trading (without hype) before moving into backtesting, simulation, paper trading, or broker-connected execution.

What should I do after reading this article?

Use the article to clarify the concept first, then review FlyTradr workflow pages such as the algo trading platform overview, methodology and assumptions, or the FAQs page before making a platform decision.