2026-06-191 min read

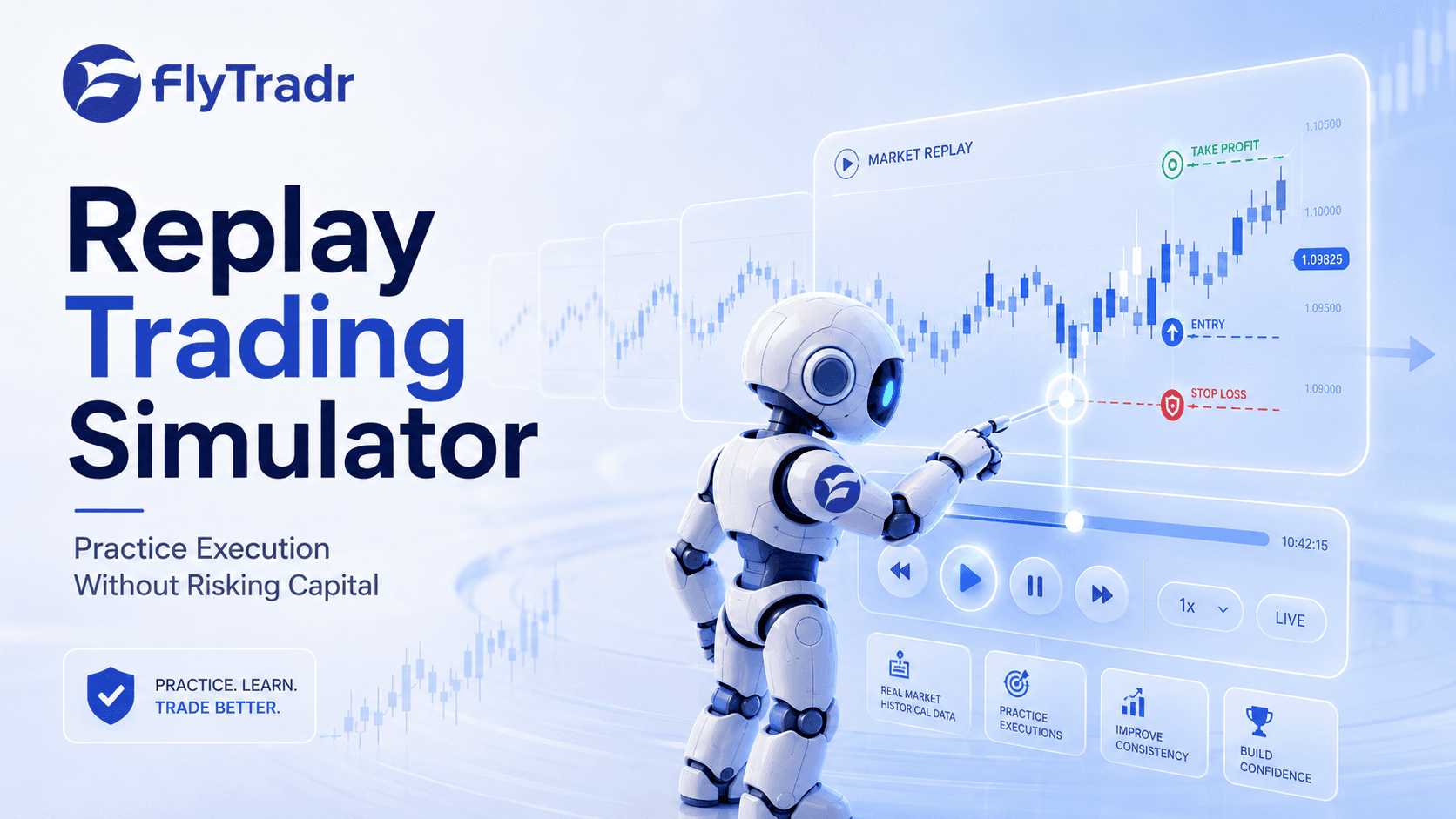

Replay Trading Simulator: How to practice execution without risking capital

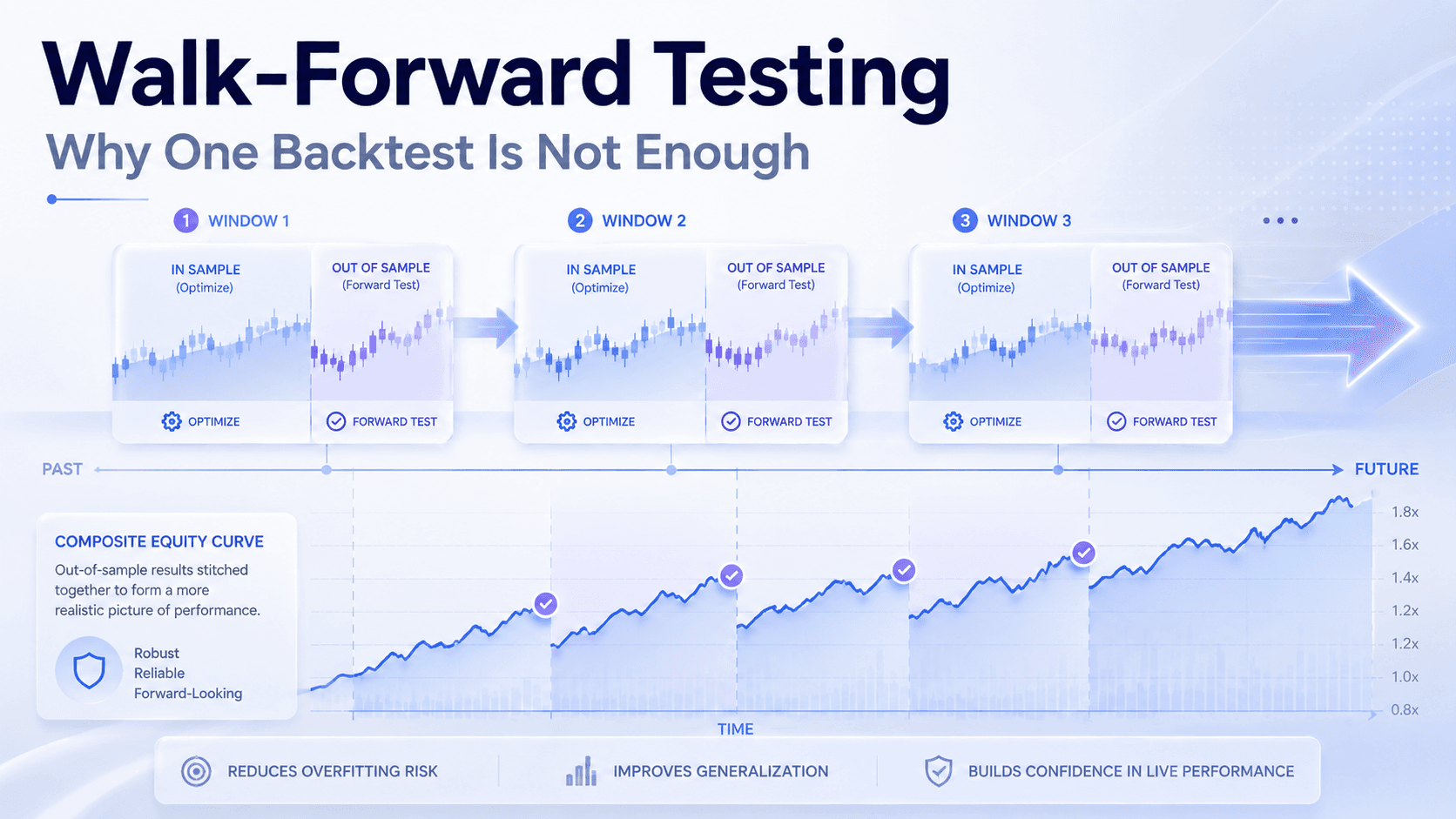

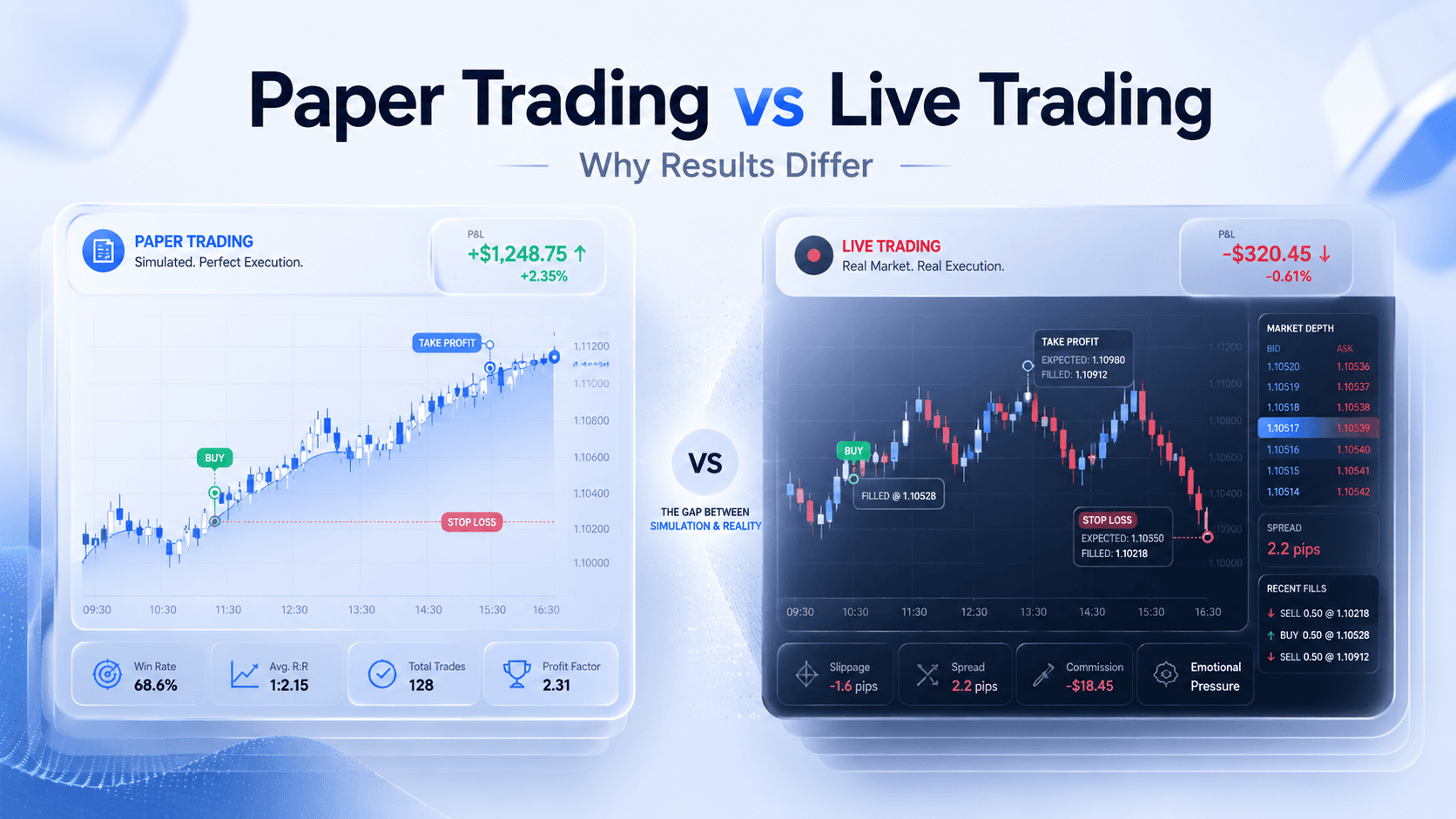

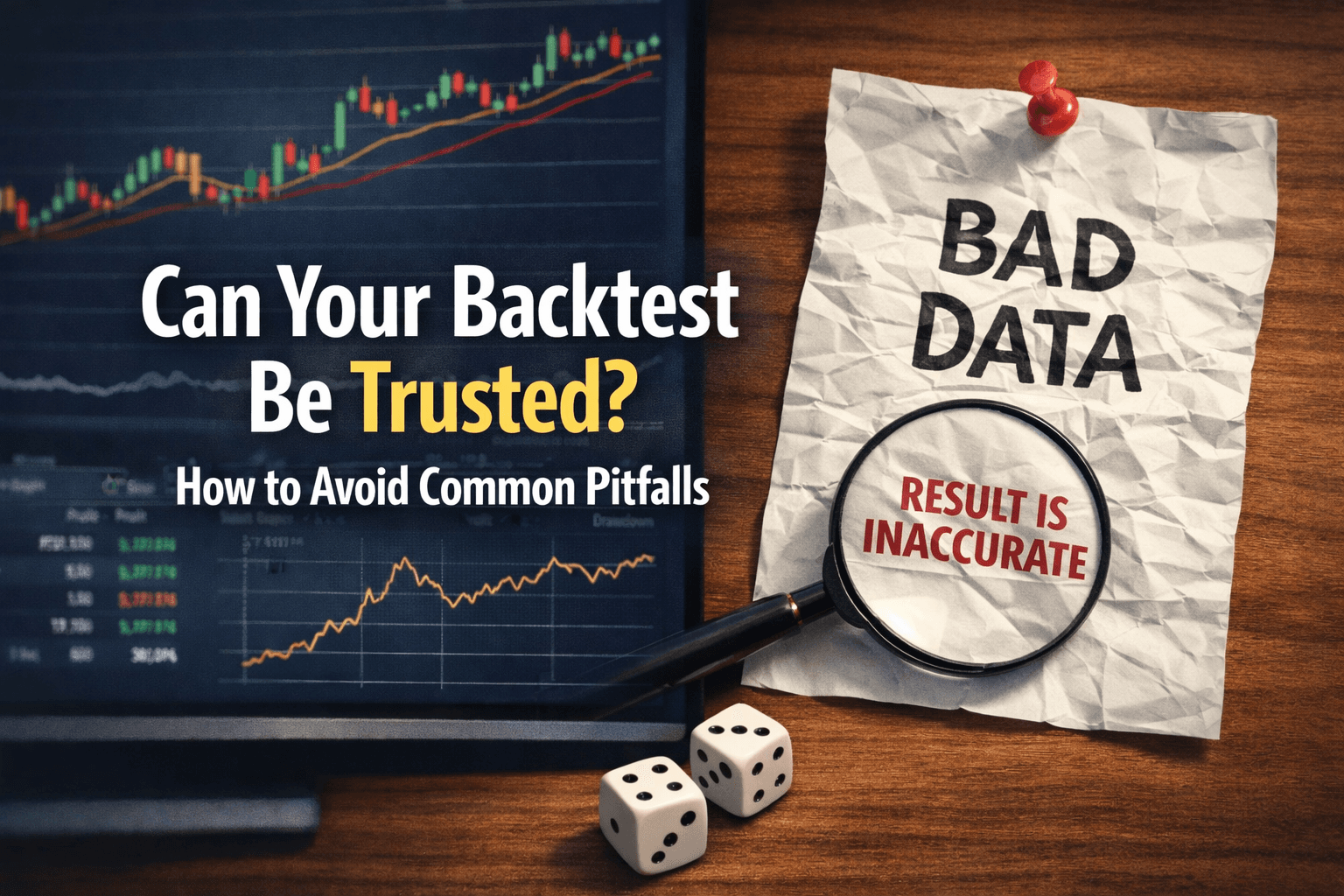

Backtests show metrics. Simulators show behaviour. Learn how market replay helps you understand how strategies actually trade before you deploy them live.

Reyaz