The best no-code workflow is not the one that hides the most complexity. It is the one that makes your strategy precise, portable, and easy to validate through backtesting, simulation, and paper trading.

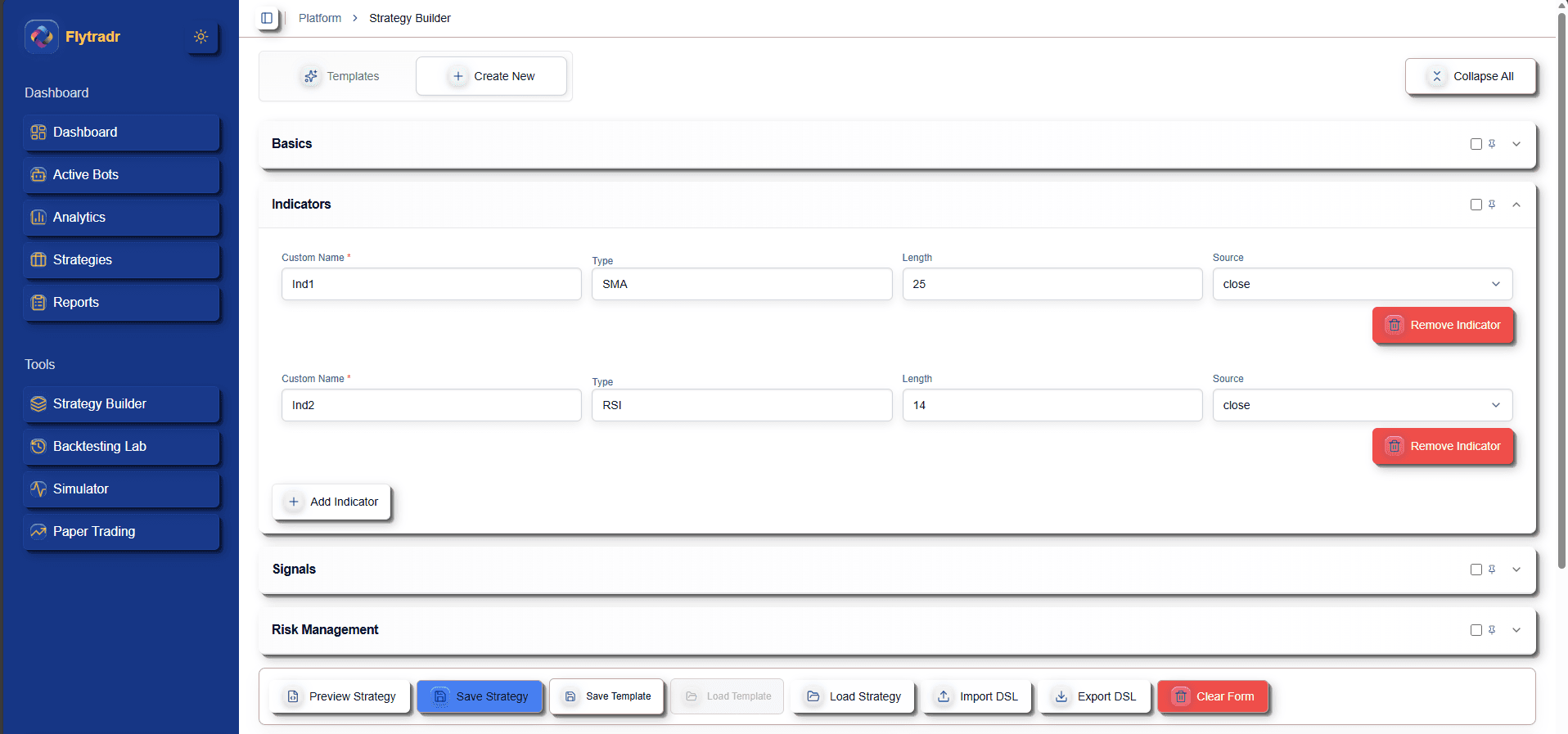

No-code is only useful if it remains explicit. FlyTradr lets you define entries, exits, indicators, filters, and risk rules visually, then compiles that logic into a validated JSON DSL. That means the strategy stays consistent across tools instead of becoming a black box.

For retail traders, that matters more than novelty. A workflow-first no-code platform should make testing clearer, not just faster.

Visual no-code strategy builder for creating algorithmic trading rules without programming.

Why the DSL matters

Many no-code products become black boxes. You can click through a flow, but you cannot verify what was actually executed, and results become hard to reproduce. With FlyTradr, the DSL is the contract: the same strategy definition powers backtests, simulation, and paper trading.

What you can build

- Rule-based entries and exits: indicator signals, price actions, filters, and conditions.

- Risk rules: position sizing, stops, take profits, max exposure, and guardrails.

- Multi-step workflows: build, backtest, simulate, and paper trade without rewriting the strategy logic.

Where to start

- Build a simple strategy with one or two indicators and basic risk rules.

- Backtest to check behavior and drawdowns.

- Simulate the worst periods to understand failure modes.

- Paper trade to validate the execution workflow.

The strongest next step after building your first strategy is to run it through backtesting, then pressure-test execution behavior in the trading simulatorbefore moving to paper trading.

Educational note: FlyTradr is not financial advice. Use it to test ideas and understand risk.

Where FlyTradr fits best

Best for

- Retail traders who want to automate strategies without learning to code first.

- Users who want one workflow from strategy design into backtesting, simulation, and paper trading.

- Traders who care about keeping strategy logic transparent across tools.

Not ideal for

- Teams looking for a code-first quant research environment.

- Traders who want to skip testing and move directly into live execution.

- Users who prefer disconnected single-purpose tools instead of one structured workflow.

Related pages

Algo trading platform

See the full FlyTradr workflow.

Best no-code algo trading platforms in India

Compare India-first no-code platform fit.

Algorithmic trading for beginners

Beginner workflow and validation basics.

FlyTradr vs Tradetron

Compare workflow clarity and trust surfaces.

FlyTradr vs Streak

India-first no-code comparison.