A trading strategy is not complete until it knows how to protect capital

Most traders spend a lot of time trying to improve their entry signal. They test indicators, adjust timeframes, compare setups, add filters, and keep looking for a cleaner way to enter the market.

That work matters, but it is only one part of trading.

A strategy is not only defined by where it enters a trade. It is also defined by what it does when the trade is wrong, how much capital it risks, how it handles losing streaks, and when it stops trading altogether.

This becomes even more important in algorithmic trading.

Automation does not make a weak strategy safer. It simply executes the rules faster and more consistently. If the rules are incomplete, automation can also make losses happen faster.

That is why risk management is not a secondary detail. It is part of the strategy itself.

Your entry signal may identify the opportunity. Your risk management decides how much damage you can take when the opportunity does not work.

Why risk management matters more in automated trading

Manual traders often rely on judgement during a trade. They may move a stop loss, close a position early, reduce size, skip a trade, or pause after a difficult session.

Sometimes that discretion helps. Sometimes it creates inconsistency.

Automated trading is different. A system follows the rules it has been given. It does not know that the trader feels nervous. It does not know that the market feels unusual. It does not hesitate because the last three trades were losses. It does not become cautious unless caution has been built into the logic.

That is why risk controls need to be defined before the trade starts.

If the system does not know where to exit, how much to risk, when to pause, and how to respond to bad conditions, then the trader has not built a complete trading strategy. They have only built an entry engine.

A serious automated strategy needs two types of rules.

Rules for finding opportunities.

Rules for protecting capital.

One without the other is incomplete.

Every trade needs a predefined exit

Every automated trade should have a clear exit plan.

This does not mean every exit must use the same type of stop loss. Some strategies use fixed percentage based stops. Some use volatility based stops. Some use indicator based exits. Some exit when the original reason for entering the trade is no longer valid.

The method can vary, but the exit should not be improvised after the trade has already gone wrong.

A mental stop loss may exist for a manual trader, although even there it is often unreliable. In automation, a mental stop loss does not exist. The system only knows the instructions it has been given.

If there is no clear exit rule, the system may hold a losing trade for too long. If the exit rule is too tight, the system may get stopped out repeatedly by normal market movement. If the exit rule is too wide, one bad trade may remove the gains from many good trades.

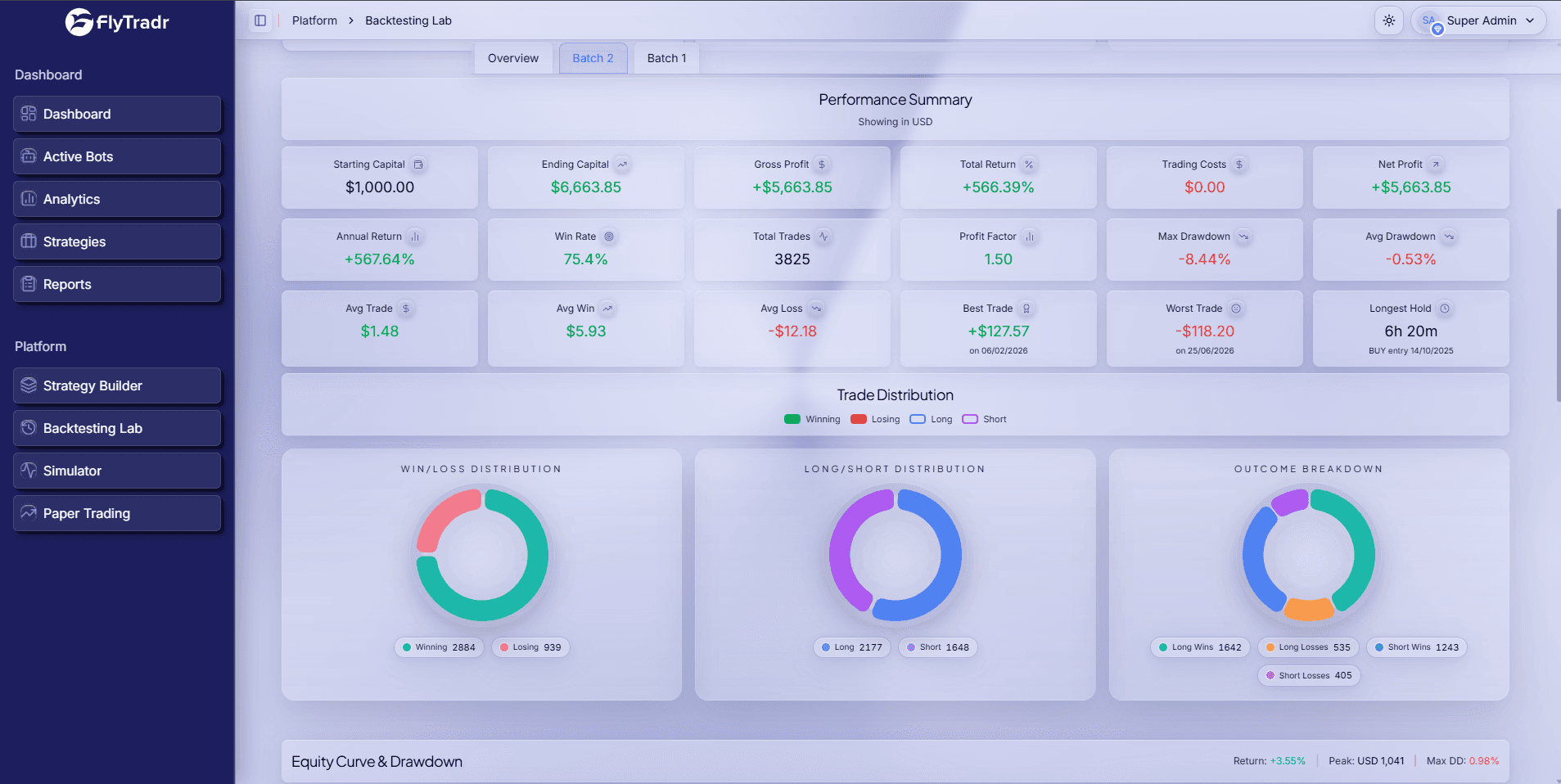

This is why the exit should be tested as carefully as the entry.

A good exit rule should answer a few practical questions.

Where is the trade idea no longer valid.

How much loss is acceptable on this trade.

Does the stop distance make sense for the volatility of the market.

Is the exit based on logic, or only on hope.

A strategy does not become safer just because it has a stop loss. It becomes safer when the stop loss makes sense for the market, the setup, and the capital being risked.

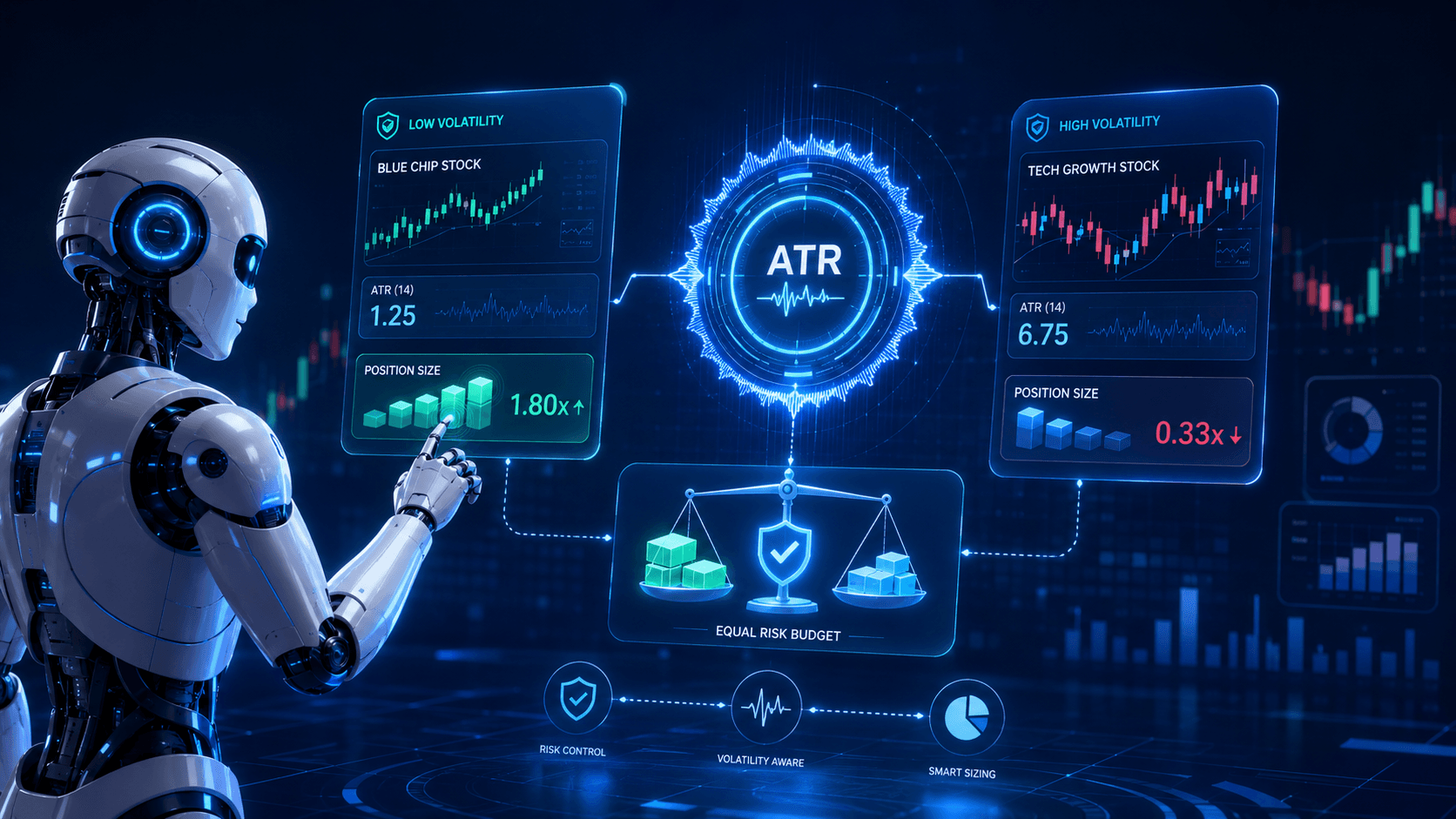

Position sizing decides how much damage one trade can do

A good entry can still become a losing trade. That is normal.

No strategy wins all the time. Losses are part of trading. The real question is whether each loss is small enough for the strategy to continue operating.

This is where position sizing matters.

Position sizing means deciding how much capital to put into a trade. More importantly, it means deciding how much capital can be lost if the trade fails.

Many traders think about position size based on confidence. If they like a setup, they take a larger position. If they are unsure, they take a smaller one. That may feel natural, but it is not a reliable risk process.

A more structured approach starts with risk first.

For example, a trader with 100000 in capital may decide that the maximum planned loss on one trade should be 1000. That is one percent of capital. The position size is then calculated around the distance between the entry price and the stop loss.

This changes the question.

The trader is no longer asking, how much can I buy.

The trader is asking, how much can I afford to lose if this trade is wrong.

That shift matters.

Two traders can take the same entry and exit, but have very different outcomes because of position sizing. One may risk a small amount and survive a losing streak. The other may risk too much and damage the account before the strategy has enough time to play out.

A strategy does not only need profitable rules. It needs survivable sizing.

Portfolio heat shows your total risk

Risk is not only about one trade.

A trader may risk two percent on a single trade and feel that the risk is controlled. But if five trades are open at the same time, and each trade risks two percent, the total planned risk is now ten percent.

This is often called portfolio heat.

In simple terms, portfolio heat means the total amount of capital currently at risk across all open positions.

This matters because trades are not always independent. A trader may think they are diversified because they have positions in different stocks. But if all those stocks belong to the same sector, or react to the same market event, they may move together.

The same issue can happen in crypto, indices, commodities, and forex. A system may open several trades that look separate, but behave like one large trade when volatility rises.

That is why automated systems need exposure limits.

A trader should know how much total capital is at risk across all open trades. They should also know whether the system is overexposed to one symbol, one sector, one market, or one direction.

A single trade can damage an account. A group of related trades can do much more.

Daily loss limits act as a circuit breaker

Even a well tested strategy can face bad conditions.

Markets change. Volatility expands. Liquidity reduces. Price action becomes noisy. A strategy that performs well in one environment may behave very differently in another.

This is why daily loss limits are useful.

A daily loss limit is a rule that pauses trading after the account loses a predefined amount in a day. It acts like a circuit breaker.

The purpose is not to predict the market. The purpose is to prevent a bad day from becoming a disastrous day.

This is especially important in automation because a system can continue executing trades even when conditions are clearly poor. A manual trader may step back after several losses. An automated system will only step back if the rule exists.

A daily loss limit can help protect the trader from unusual conditions, technical issues, poor execution, and strategy behaviour that no longer matches the backtest.

It is not a perfect solution, but it creates a boundary.

And in trading, boundaries matter.

Costs must be part of the test

A strategy can look profitable before costs and fail after costs.

This is one of the most common problems in backtesting.

Trading costs include brokerage, exchange charges, taxes, spreads, and slippage. Slippage means the difference between the expected price and the actual price received.

These costs may look small on a single trade. But over many trades, they can change the entire result.

This matters most for strategies that trade frequently or aim for small profits per trade. If a strategy makes a small average profit on each trade, even modest costs can remove the edge.

A backtest that ignores costs may show a smooth equity curve, but the live result may be very different.

This is why realistic testing is essential.

A trader should not only ask whether the strategy was profitable in the backtest. They should ask whether it was profitable after realistic costs.

If the strategy only works when costs are ignored, it probably does not work in practice.

Infrastructure is also part of risk

Many traders think of risk only in market terms.

They think about price risk, drawdown risk, position risk, and leverage risk. Those are important, but algorithmic trading also has operational risk.

A strategy can be logically sound and still fail because the execution setup is weak.

There are several practical questions traders should consider before going live.

What happens if the internet connection fails.

What happens if the system crashes.

What happens if an order is placed twice.

What happens if a stop order is not placed correctly.

What happens if broker connectivity becomes unstable.

What happens if API access or broker rules change.

These are not small technical details. They are part of the real trading environment.

For Indian traders, this conversation has become more important as the regulatory framework around retail algorithmic trading has become more structured. SEBI issued a circular on February 4, 2025, covering safer participation of retail investors in algorithmic trading, including broker controls, API based access, order traceability, and exchange level oversight. SEBI later issued an extension circular on September 30, 2025, giving brokers and related participants more time for implementation.

The practical takeaway is simple. Algo trading is not only about strategy logic. It is also about secure access, reliable execution, traceable orders, and controlled deployment.

Traders do not need to become compliance experts to understand this. But they should understand that live automation needs a serious operating environment.

A trading bot running without clear controls is not professional automation. It is unmanaged execution.

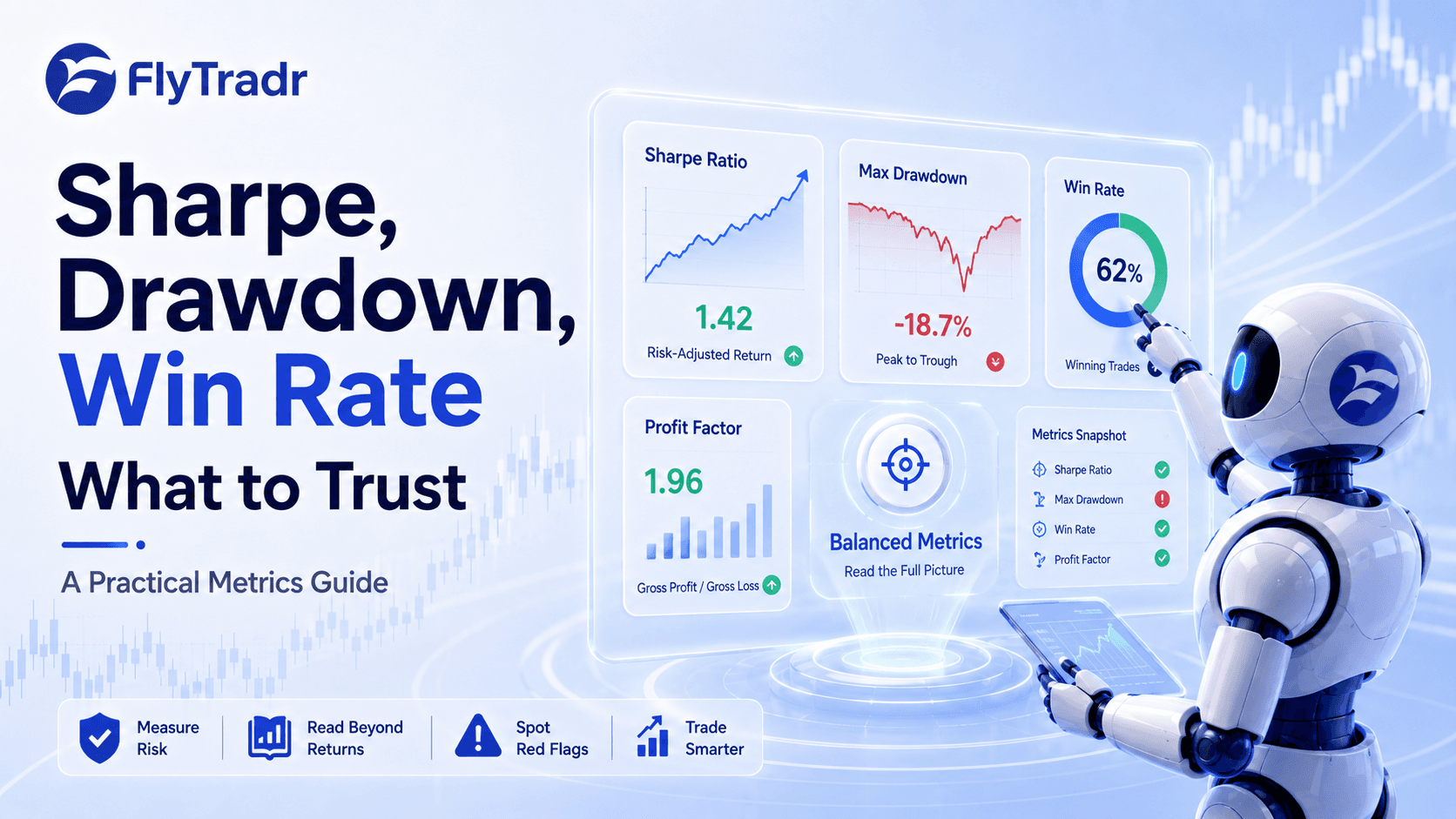

Risk management should be tested before real money is involved

The best time to test risk logic is before capital is at risk.

Backtesting helps you understand how the strategy behaved in the past. Paper trading helps you observe how the strategy behaves in real time without risking money. Live trading should come only after the trader understands the strategy, the drawdowns, the execution assumptions, and the risk controls.

This staged approach matters.

A trader should not move from idea to live trading just because a backtest looks good. They should test whether stop losses behave as expected. They should check whether position sizing works correctly. They should observe whether daily limits trigger properly. They should review whether the system handles losing streaks in a controlled way.

Risk logic should be tested like strategy logic.

It is not enough for the system to know when to enter. It must also know when to exit, when to reduce risk, and when to stop.

The mindset shift, from profit first to survival first

Many traders begin with the question, how much can I make.

That is understandable. Everyone enters the market for returns.

But serious trading starts with a different question.

How much can I afford to lose if I am wrong.

This question does not sound exciting, but it is more useful. It forces the trader to think about downside first. It makes position sizing more disciplined. It makes drawdowns easier to evaluate. It helps prevent one trade, one day, or one market condition from causing excessive damage.

Risk management does not guarantee profit.

Nothing does.

But it helps prevent avoidable failure.

A trader who protects capital has the chance to keep learning, testing, improving, and executing. A trader who ignores risk may not stay in the game long enough for any edge to matter.

What traders should review before going live

Before moving a strategy into live execution, traders should review the full risk structure.

The exit logic should be clear.

The risk per trade should be defined.

The position sizing method should be consistent.

The maximum daily loss should be known.

The total portfolio exposure should be limited.

Fees and slippage should be included in testing.

The strategy should be tested across different market conditions.

The trade log should be reviewed for strange behaviour.

The system should be tested in a paper trading or virtual environment.

The trader should know what kind of drawdown would make them pause, review, or stop the strategy.

This process may feel slower, but slower is often safer.

The goal is not to rush into automation. The goal is to understand what is being automated.

Final thought

In trading, the entry signal gets most of the attention. Risk management usually gets less.

But over time, risk management is what decides whether a strategy can survive.

A good strategy does not only find trades. It controls losses, sizes positions sensibly, limits exposure, stops during bad conditions, accounts for costs, and operates within a reliable execution setup.

That is the real edge.

Not because risk management guarantees returns. It does not.

But because without risk management, even a good idea can fail before it has enough time to prove itself.

In algorithmic trading, speed and automation are powerful only when they are controlled.

The goal is not just to build a system that can trade. The goal is to build a system that knows how much it is allowed to lose, when it should step back, and how it can survive long enough for its logic to matter.

Comments

Ask a question or leave feedback. Guests can post too.

Max 2000 characters.

No comments yet.

Quick answers

What is this article about?

A trading strategy finds the opportunity, but risk management ensures you survive to profit from it.

Who should read this article on Beyond the Strategy, Why Risk Management Is Your Real Edge?

This article is for retail traders who want a practical understanding of beyond the strategy, why risk management is your real edge before moving into backtesting, simulation, paper trading, or broker-connected execution.

What should I do after reading this article?

Use the article to clarify the concept first, then review FlyTradr workflow pages such as the algo trading platform overview, methodology and assumptions, or the FAQs page before making a platform decision.