Backtesting is the process of running strategy rules on historical market data to estimate how the strategy would have behaved under defined assumptions. It is useful, but it is not proof.

A backtest turns a trading idea into something inspectable. Instead of relying on memory or intuition, you can see how the rules would have behaved over past market periods.

That makes backtesting useful for learning and validation. It does not make it predictive certainty. The quality of the assumptions matters as much as the result itself.

Backtesting is most useful when the assumptions and risk profile are visible, not hidden behind a single return number.

How backtesting works

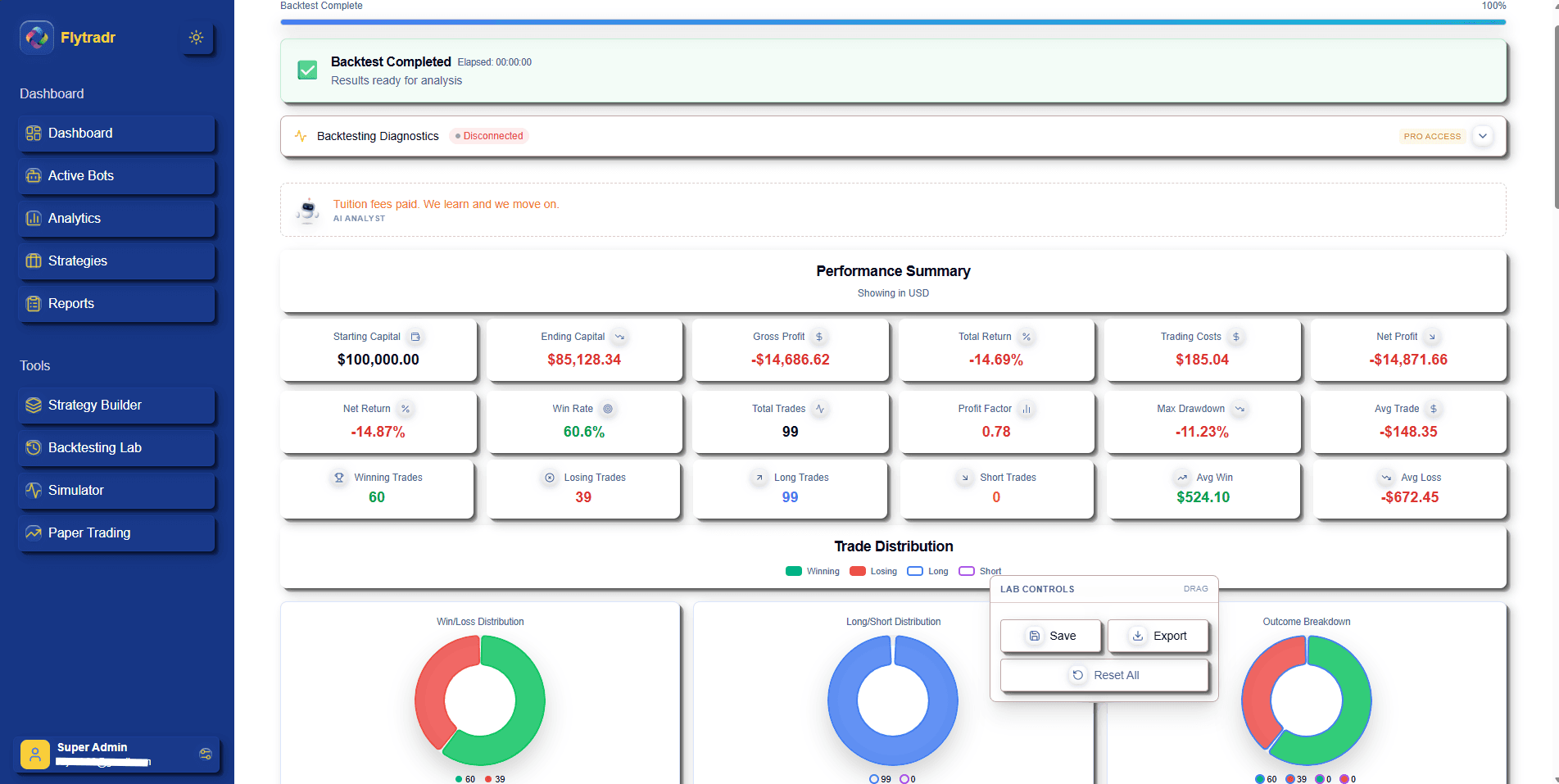

- You define exact rules for entries, exits, risk, and position sizing.

- You run those rules on historical price data.

- You include assumptions such as fees, slippage, and timing.

- You inspect drawdowns, trade distribution, and stability across conditions.

- You decide whether the idea deserves further testing in simulation and paper trading.

What can go wrong in a backtest

- Overfitting: optimizing rules too closely to the past.

- Ignored friction: missing fees, slippage, or latency.

- Bad data assumptions: poor data quality or survivorship bias.

- Weak risk review: focusing on returns while ignoring drawdown behavior.

What a retail trader should do next

Treat the backtest as a first filter. If the idea looks promising, continue with the broader algo trading platform workflow, then move into a simulation workflow and then paper trading. That sequence gives you a more honest picture than historical results alone.

Who should use backtesting carefully

Best for

- Retail traders who want to pressure-test a rules-based trading idea before risking capital.

- Beginners who need to learn the difference between historical validation and live behavior.

- Traders who want to inspect risk, drawdown, and trade distribution rather than only P and L.

Not ideal for

- Anyone looking for guaranteed performance from historical data alone.

- Users who want to skip execution assumptions and still trust the result.

- Traders who treat one strong backtest as enough proof to go live immediately.

Related pages

Algo trading platform

See the full FlyTradr workflow.

Backtesting software

FlyTradr product page for historical validation.

Trading simulator

The next stage after a backtest.

Paper trading

Forward validation with virtual capital.

FlyTradr AI

Learn how the assistant can explain supported testing context without predicting results.

What is algorithmic trading

The wider category explainer.

Learn hub

Browse more educational pages.