Why Strategies Work on 1D but Fail on 1m: Timeframe Traps Explained

You backtest a trading strategy on daily (1D) bars and see these metrics:

Total return: 45%

Sharpe ratio: 1.8

Max drawdown: 14%

Your immediate reaction: "This is it. I’ve found the holy grail."

Eager to capture more signals and accelerate your returns, you switch the exact same strategy to 1-minute (1m) bars.

The devastating reality check:

Total return: -12%

Sharpe ratio: 0.3

Max drawdown: 28%

What happened? You fell straight into a timeframe trap.

In this guide, we will unpack:

Why identical strategies perform drastically differently across timeframes.

The 5 most common timeframe traps (and exactly how to avoid them).

How to mathematically and logically choose the right timeframe for your system.

The structural changes that occur when scaling your trading logic up or down.

Why Timeframe Matters

A timeframe represents the specific duration of a single price bar or candle on your chart.

Long-term: Daily (1D), Weekly (1W), Monthly (1M)

Swing: 4-hour (4H), 1-hour (1H)

Intraday: 15-minute (15m), 5-minute (5m), 1-minute (1m)

Scalping: 30-second (30s), tick-by-tick

Think of timeframes as different lenses looking at the exact same market:

The 1D chart provides a macro lens, filtering out daily volatility to reveal sweeping trends and major structural reversals.

The 1m chart provides a microscopic lens, exposing every minor price fluctuation, bid-ask bounce, and algorithmic flicker.

Different lenses don't just reveal different opportunities—they introduce entirely different structural risks.

The 5 Biggest Timeframe Traps

Trap 1: Noise Overwhelms Signal

On a 1D chart, price movements are generally meaningful, driven by fundamental shifts, corporate earnings, and major institutional flows. On a 1m chart, price movements are largely chaotic noise driven by high-frequency market-making and localized order book imbalances.

The Indicator Disconnect:

Daily RSI < 30: Occurs 5 to 10 times a year. It usually signals genuine macro oversold conditions and is frequently followed by multi-day rallies.

1-Minute RSI < 30: Occurs 50+ times a day. It is often just a temporary structural dip followed by immediate consolidation or a continuation downward. There is rarely meaningful macro follow-through.

Why it happens:

Lower timeframes provide exponentially more data points, but a drastically lower signal-to-noise ratio.

Analogy: Reading a 1D chart is like studying the ocean's tide; reading a 1m chart is like trying to predict the trajectory of individual, chaotic waves.

How to avoid it:

Never extrapolate: Backtest your strategy exclusively on the exact timeframe you plan to execute.

Implement structural filters: Add trend-following or volume-based filters (e.g., VWAP or moving averages) to screen out low-probability intraday noise.

Incorporate macro context: Only take 1m execution signals if they align with the higher-timeframe (e.g., 1H or 1D) structural trend.

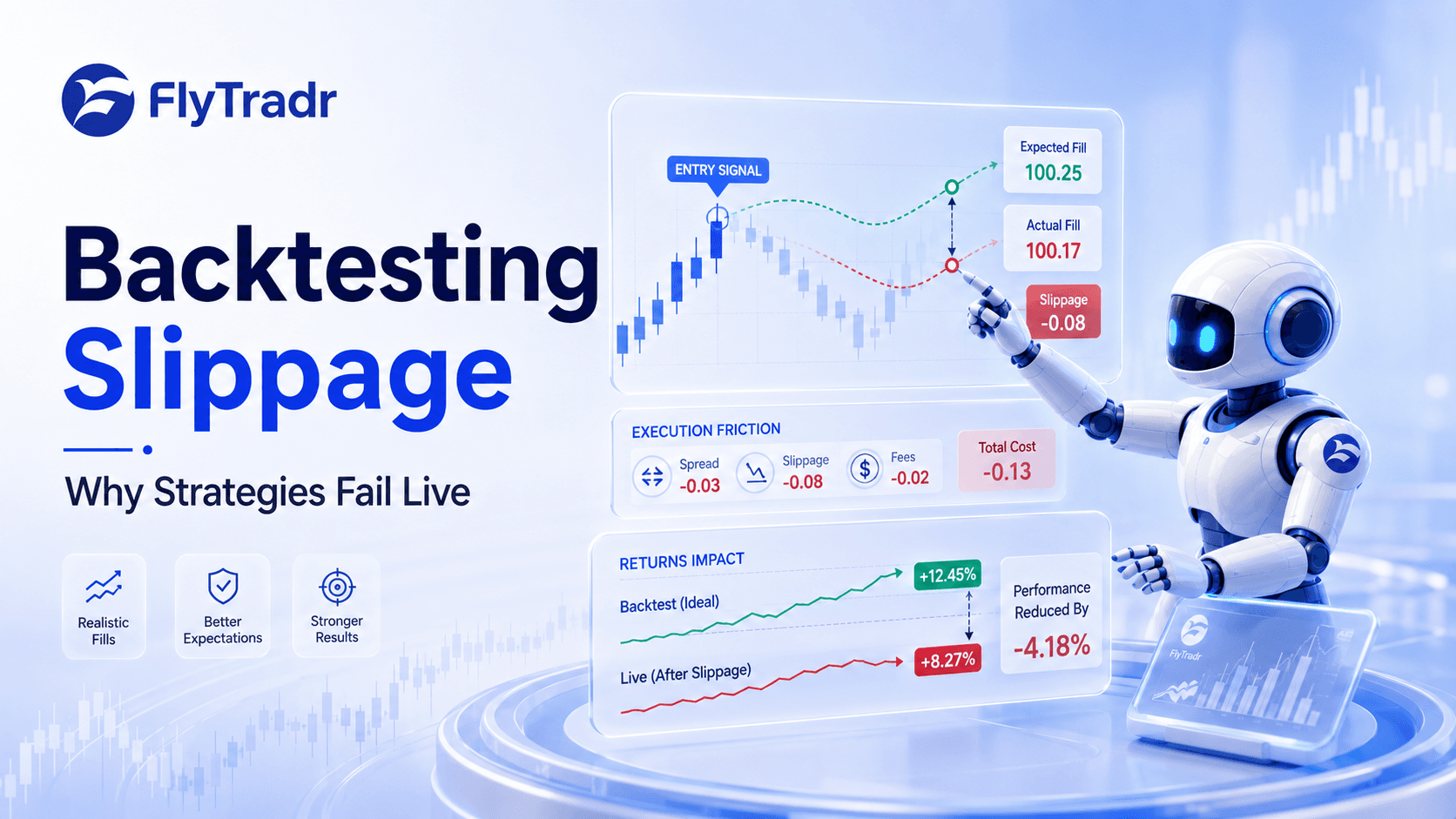

Trap 2: Frictional Execution Costs Destroy Profits

A strategy that trades rarely can afford loose execution; a strategy that trades constantly will bleed out from frictional costs.

Metric | Daily (1D) Framework | 1-Minute (1m) Framework |

Trades per Year | 50 | 500 |

Avg. Slippage per Trade | $0.05 | $0.05 |

Total Annual Slippage | $2.50 (Negligible) | $25.00 (Severe) |

Commissions ($1/trade) | $50.00 | $500.00 |

If your strategy's average gross profit per trade is $10.00, slippage and commissions consume a tiny fraction of your returns on the 1D timeframe. On the 1m timeframe, those exact same fixed overhead costs will aggressively pull a winning strategy into deep unprofitability.

Why it happens:

Lower timeframes trigger a higher frequency of trading signals. High frequency multiplies your compounding execution drag (spread, slippage, and fees).

How to avoid it:

Inject realism into your backtests: Always model realistic slippage (at least $0.05 to $0.10 per share/contract for market orders) and actual broker commission schedules.

Enforce a cost-per-trade threshold: Use the following quick formula to check viability:

$$\text{Minimum Profitable Target} = 2 \times \text{Total Frictional Execution Costs}$$

If your total transaction cost (slippage + commission) is $1.05 per trade, your strategy must average a gross profit of at least $2.10 just to be statistically viable. If your 1m strategy only captures a gross average of $1.50, you are simply funding your broker.

Trap 3: Overfitting to Intraday Statistical Flukes

Data volume is a double-edged sword. While more data allows for robust testing, it also creates an environment ripe for historical data-mining.

Daily Data (5 Years): ~1,250 bars.

1-Minute Data (5 Years): ~600,000+ bars.

With over half a million data points, optimization engines can easily find highly complex, purely coincidental patterns that look flawless in a backtest but fail instantly in live markets.

Example of an over-optimized rule: "Buy when price dips 0.3% below VWAP between 10:17 AM and 10:23 AM, but only if volume is precisely 1.4x the rolling average."

Why it happens:

If you flip a coin 10,000 times, you are mathematically guaranteed to see a streak of 10 heads in a row at some point. An overfitted algorithmic strategy treats that random statistical anomaly as a predictable, repeatable law.

How to avoid it:

Rigorous out-of-sample testing: Use a strict walk-forward optimization process. Optimize parameters on 60% of your data, and validate it on the remaining 40% of untouched data.

Embrace simplicity: Limit the number of parameters or indicator inputs in your logic. Fewer variables directly equate to less curve-fitting.

Trap 4: Latency and Execution Delays

On a daily chart, a 2-second delay in order routing is irrelevant—the closing price won't drastically shift in the final moments. On a 1m chart, a 2-second delay completely mutates your risk profile.

The Momentum Problem:

Suppose your 1m momentum strategy triggers a "Buy" market order the millisecond price breaks a key local resistance level at $450.00.

Backtest Assumption: You get filled instantly at $450.00.

Live Execution Reality: By the time your signal processes, routes to the exchange, and matches with an order book, the price has surged to $450.15.

You just absorbed 15 cents of negative slippage. Across hundreds of rapid trades, this structural lag completely erases your edge.

How to avoid it:

Build a latency buffer: Explicitly program a 1-to-3 second execution delay into your backtesting engine to see if the edge survives realistic fills.

Utilize limit orders: Wherever possible, use marketable limit orders to establish a hard cap on your maximum acceptable entry price.

Avoid ultra-low timeframe momentum: Unless you are co-located with an exchange and running institutional-grade execution infrastructure, steer clear of sub-5-minute pure breakout strategies.

Trap 5: Intraday Structural Decay

Macro economic trends can persist for decades because human behavior and corporate performance shift slowly. Conversely, intraday patterns are incredibly fragile.

Intraday edges are typically driven by structural inefficiencies: localized market-maker inventory adjustments, specific institutional execution algorithms, or predictable retail order flows. The moment a major high-frequency trading (HFT) firm alters its execution routing logic or a broker changes its payment for order flow (PFOF) rules, your intraday pattern can vanish permanently.

How to avoid it:

Expect a shorter strategy lifespan: While a solid 1D macro trend strategy can function reliably for 5+ years, a sub-15m intraday strategy often requires re-tuning or decommissioning every 6 to 12 months.

Perform quarterly robustness audits: Continually re-verify your intraday models against fresh out-of-sample data quarterly to detect early signs of edge decay.

How to Choose the Right Timeframe

1. Match Timeframe to Strategy Type

Select a timeframe suited to the underlying mechanics of your trading system:

Strategy Type | Best Timeframe | Rationale |

Trend Following | Daily (1D), 4-Hour (4H) | Structural macroeconomic trends require time and volume to mature. |

Mean Reversion | 1-Hour (1H), 15-Minute (15m) | Functions best within defined, range-bound intraday cycles. |

Breakout | Daily (1D), 1-Hour (1H) | Requires highly liquid, clear structural levels of support and resistance. |

Momentum | 15-Minute (15m), 5-Minute (5m) | Captures clean, rapid acceleration windows while keeping trading costs manageable. |

Scalping | 1-Minute (1m), Ticks | Hyper-fast execution targeting micro-inefficiencies; requires ultra-low latency. |

2. Match Timeframe to Holding Period

As a foundational rule of thumb:

$$\text{Target Holding Period} = 5 \text{ to } 10 \times \text{Signal Timeframe}$$

If your entry signal is triggered on a 1-minute chart, your optimal holding period should be roughly 5 to 10 minutes.

Using 1-minute bars to establish a position you intend to hold for 3 weeks introduces immense local noise without providing any structural advantage. Conversely, using a 1D chart to execute a 10-minute scalp lacks the granular precision required to manage risk.

3. Match Timeframe to Available Capital

Your account size dictates your resilience to frictional transaction drag:

Under $5,000: Stick to Daily (1D) or 4H charts. Your priority is maximizing your edge per trade while aggressively minimizing commissions and spread costs.

$5,000 – $25,000: 1H and 4H charts offer a moderate trading frequency that won't compound transaction fees faster than your account can scale.

$25,000 – $100,000: 15m and 5m charts become highly viable, as your position sizes can comfortably absorb standard execution frictions.

$100,000+: 1m and sub-minute charts are clear options, provided you utilize professional, low-cost direct market access (DMA) brokerages.

How to Responsibly Adapt Strategies Across Timeframes

If you have a viable macro strategy that you want to scale down to lower timeframes, do not simply copy and paste the parameters. Implement these four structural adaptations:

1. Dynamically Adjust Indicator Periods

Lower timeframes require more responsive indicators to successfully capture faster price cycles.

Example: If you use a standard RSI(14) on a 1D chart, consider tightening it to an RSI(9) or RSI(7) when operating on a 15m chart to keep the indicator sensitive to fast-moving localized adjustments.

2. Stack Confirmation Filters

Where a single technical trigger might suffice on a 1D chart, lower timeframes require absolute confluence to filter out noise.

Instead of just: Buy when RSI < 30.

Use: Buy when RSI < 30 AND price is trading cleanly above VWAP (intraday trend confirmation) AND current volume is > 1.5x the rolling average (liquidity/momentum confirmation).

3. Symmetrically Scale Down Stops and Targets

Your risk management architecture must contract proportionally to your timeframe's average true range (ATR).

Daily Strategy Setup: Stop Loss: -5.0% | Profit Target: +10.0%

1-Minute Strategy Setup: Stop Loss: -0.5% | Profit Target: +1.0%

4. Implement Multi-Timeframe Analysis

Always use a higher-timeframe anchor for directional bias, and a lower-timeframe chart for precise execution execution.

Macro Anchor (1D Chart): Confirm the dominant market bias (e.g., Ensure asset is trading above its 200-period Moving Average).

Intermediate Anchor (1H Chart): Pinpoint local pullbacks or structural support areas.

Execution Anchor (15m/5m Chart): Trigger your exact order entry the moment local momentum shifts back in favor of the macro trend.

Testing Timeframe Transitions in FlyTradr

FlyTradr’s Backtesting Lab allows you to effortlessly benchmark a single strategic thesis across multiple asset timeframes.

Recommended Validation Workflow:

Establish your baseline: Build and test your core logic on daily (1D) bars first.

Step down gradually: Shift the exact same logic down to 4H bars, then 1H bars, systematically monitoring how your core performance metrics respond.

Audit the decay: Continue stepping down to 15m, 5m, and 1m intervals.

Critical Metrics to Compare:

Sharpe / Sortino Ratios: Does your risk-adjusted return decay rapidly as you drop timeframes?

Max Drawdown: Does your peak-to-trough equity drop expand unsustainably on intraday data?

Average Profit per Trade: Is your net profit per trade comfortably scaling past 2x your estimated execution frictions?

⚠️ Red Flag Alert: If your Sharpe ratio drops by more than 50% or your maximum drawdown doubles when migrating from a 1H chart to a 5m chart, your strategy does not possess a structural intraday edge. Cease scaling down and keep your capital deployed on the higher timeframe.

Summary

Lower timeframes do not simply represent a smaller, faster version of the market—they change the game entirely. When you shift from a macro daily chart to an intraday 1-minute chart, you are stepping out of an environment governed by long-term trends and into a complex arena dominated by high-frequency market mechanics, severe frictional drag, and heavy noise.

Never assume a daily strategy will function intraday without incorporating multi-timeframe filters, modeling realistic execution friction, and managing parameters for shorter strategy lifespans.

Ready to find your strategy's optimal timeframe profile? Benchmark your system safely using FlyTradr's Backtesting Lab today. Explore our professional features and data feeds at FlyTradr.

Comments

Ask a question or leave feedback. Guests can post too.

Max 2000 characters.

No comments yet.

Quick answers

What is this article about?

Your strategy backtests beautifully on daily charts but collapses on 1-minute data.

Who should read this article on Why Strategies Work on 1D but Fail on 1m: Timeframe Traps Explained?

This article is for retail traders who want a practical understanding of why strategies work on 1d but fail on 1m: timeframe traps explained before moving into backtesting, simulation, paper trading, or broker-connected execution.

What should I do after reading this article?

Use the article to clarify the concept first, then review FlyTradr workflow pages such as the algo trading platform overview, methodology and assumptions, or the FAQs page before making a platform decision.